EBITDA is a state of mind

.avif)

"𝙐𝙣𝙘𝙖𝙥𝙥𝙚𝙙" is the holy grail for borrowers—not so much for lenders.

Manipulation of EBITDA through cost savings addbacks can increase a borrower’s ability to incur priming debt, move assets from the credit group via dividends or asset transfers, or even avoid an event of default under a financial covenant.

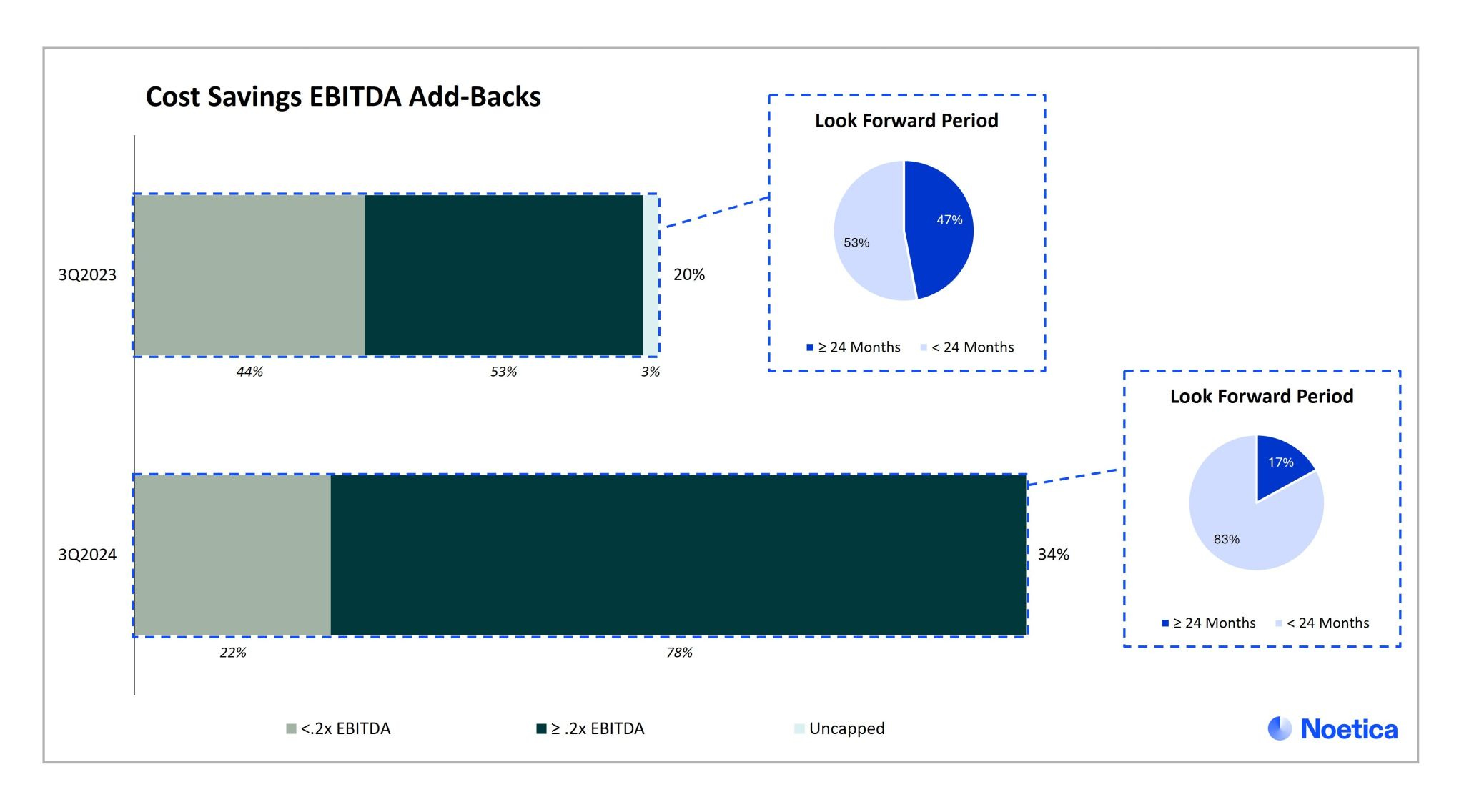

While uncapped addbacks remain relatively rare, high caps and long look-forward periods still provide significant flexibility for borrowers. In the third quarter of 2024, 34% of publicly filed high yield credit agreements permitted cost savings-based addbacks to EBITDA, compared to only 20% of such deals in the same period in 2023.

Of deals allowing such add-backs, none permitted uncapped addbacks in Q3 2024, compared to 3% in Q3 2023.

However, in Q3 2024, 78% of deals permitting cost savings addbacks included caps equal to or greater than 20% of EBITDA, compared to 53% of such deals in Q3 2023. In addition, 17% of such deals in Q3 2024 included a look-forward period of 24 months or greater, compared to 47% of Q3 2023.

Message me if you’d like access to the deal data underlying the EBITDA addbacks.

.avif)