Net shorts were supposed to be a big deal. Then everyone moved on.

.avif)

The smallest misstep leading to technical default can have cascading effects: possibly resulting in the implosion of a debt stack.

Since the Windstream bankruptcy in 2019, which was triggered by a hedge fund with a net short position successfully arguing that a years-old sale-leaseback deal violated bond covenants, borrowers have introduced protections from "net short" holders and manufactured defaults through the introduction of:

- "Anti-net short holder" language and

- The inclusion of temporal limitations on events of default

At the time, conventional thinking was that these protections would become standard in credit deals. Not only have they not become standard, but they are becoming less prevalent.

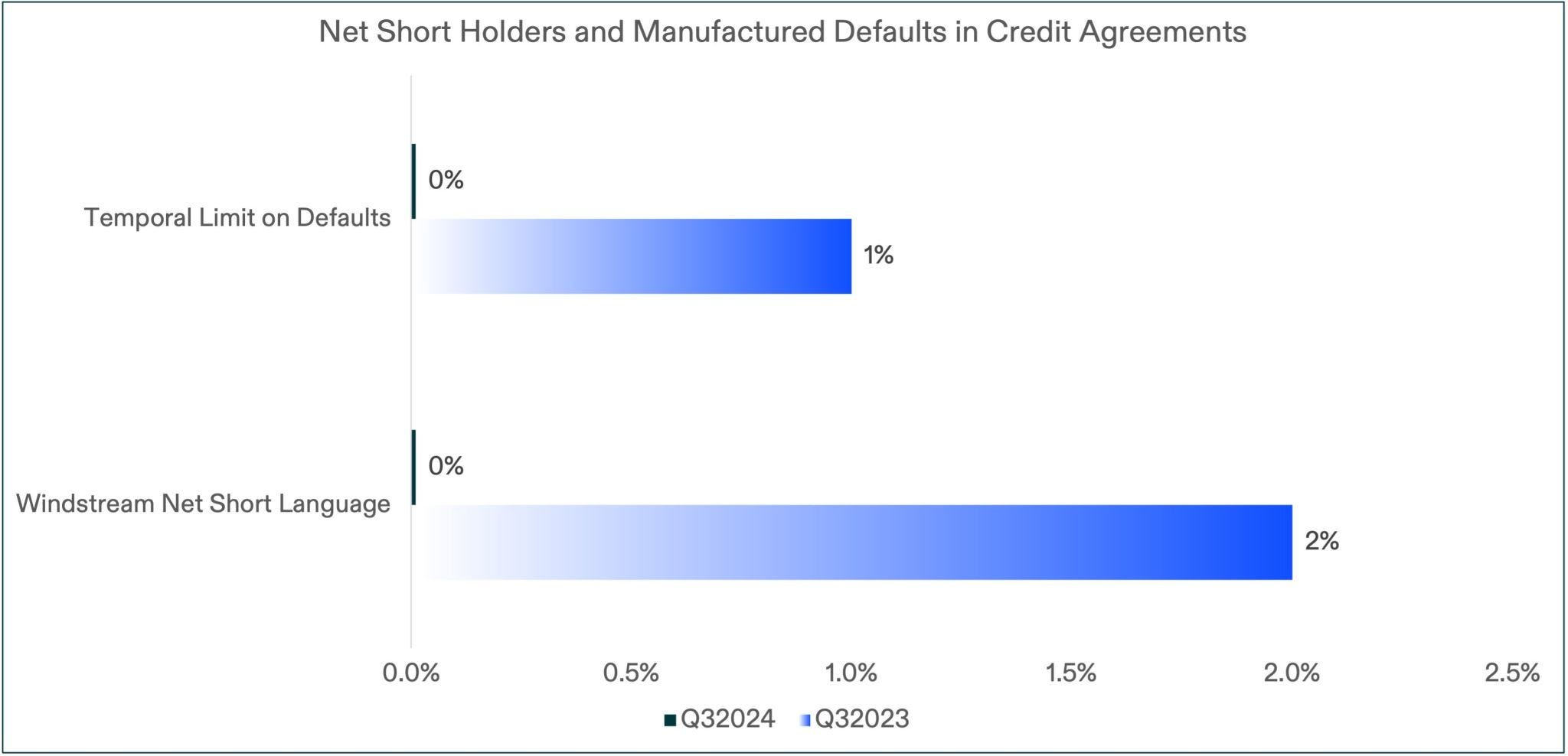

In the third quarter of 2024, no publicly filed high yield credit agreements included Windstream net short holder protections or temporal limitations on default. By comparison, 2% of similar documents filed in the same period of 2023 included net short holder protections, and 1% included temporal limitations on default. Will these borrower protections become a thing of the past?

Message me if you’d like access to deal data underlying the chart on net short protections and temporal limitations on default.

.avif)