Sell the front door, keep the house

.avif)

What if you could stop paying your mortgage, and keep your house, just by selling your front door? Welcome to the world of “𝗔𝘂𝘁𝗼𝗺𝗮𝘁𝗶𝗰 𝗚𝘂𝗮𝗿𝗮𝗻𝘁𝗲𝗲 𝗥𝗲𝗹𝗲𝗮𝘀𝗲𝘀” in corporate credit.

When someone takes out a mortgage to buy a house the basic arrangement is pretty simple: make payments on the mortgage and the bank doesn’t foreclose on the house. But what if the mortgage agreement also said something unique: “if any part of the house is sold, the bank loses its ability to foreclose on the house altogether.” Well then, the homeowner’s negotiating leverage becomes pretty obvious: sell the front door, stop paying the mortgage, and keep the house.

“Automatic guarantee releases” release subsidiary guarantors from their guarantees when they cease being wholly owned by the credit group. In many cases, all it takes is the transfer of a single share of subsidiary stock for lenders to lose a significant portion of their credit support.

However, certain deals include “anti-PetSmart”1 terms, which:

- Restrict the automatic release of non-wholly-owned subsidiary guarantors, or

- Require that any transactions that result in non-wholly-owned subsidiaries have a bona fide business purpose.

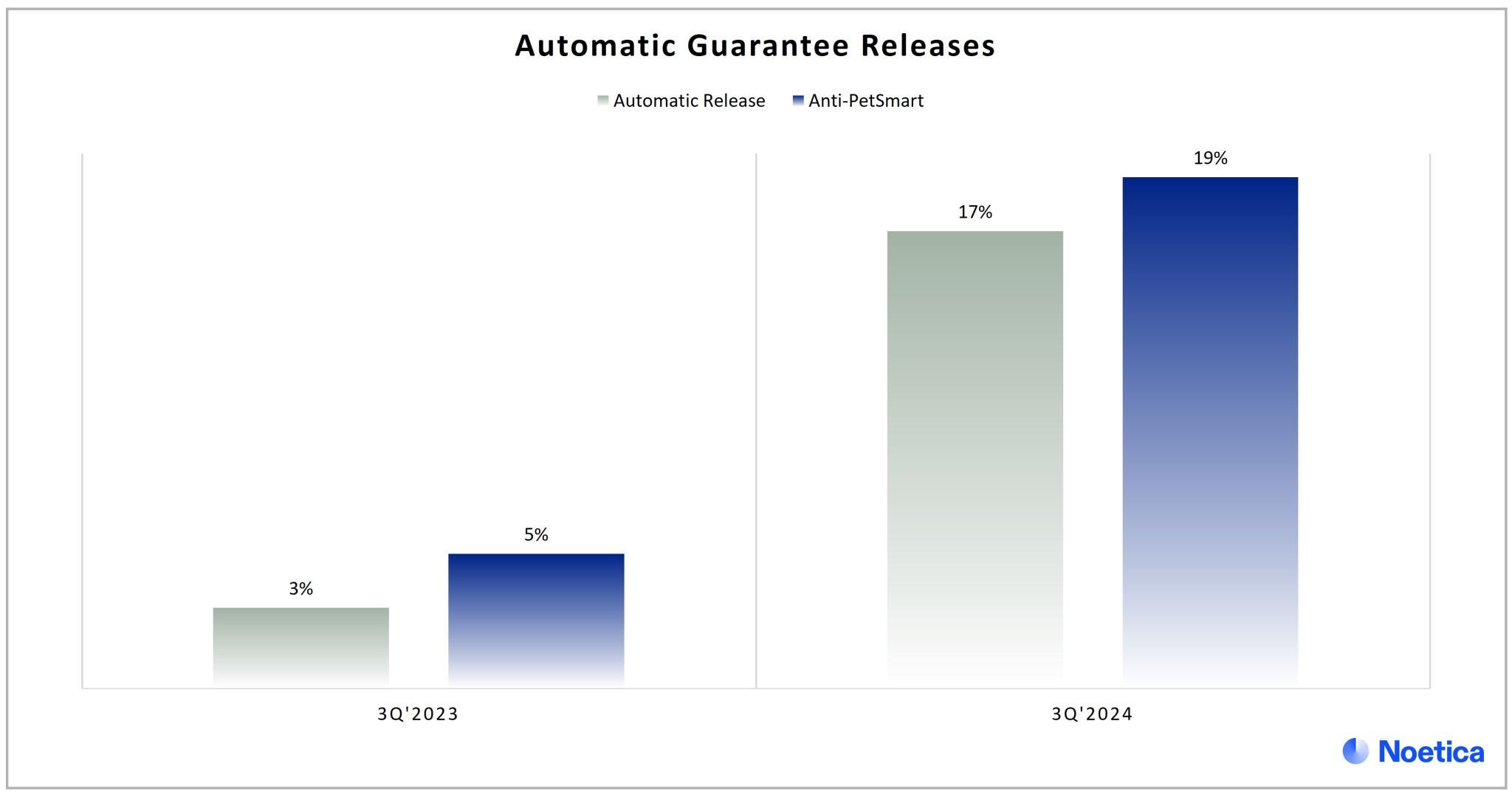

In Q3 ‘24, 17% of publicly filed high yield credit agreements automatically released subsidiary guarantors that ceased to be wholly-owned, a notable increase from 3% during the same quarter in 2023.

This increase in automatic releases, however, was matched by an increase in anti-PetSmart terms. In Q3 ‘24, 19% contained protective terms, while 5% contained the same terms in Q3 ‘23.

Message me if you’d like access to the Excel with deal data on “anti-PetSmart” terms.

1. In 2018, PetSmart quietly moved a large stake in its valuable subsidiary Chewy out of the credit group, using loopholes in its loan documents to strip collateral from lenders—sparking widespread outrage and the rise of “anti-PetSmart” protections.

.avif)