This is your captain speaking: we've begun our descent into structural subordination

.avif)

If you’re anything like me, when you see someone running for their flight at the airport, you routinely give them permission to cut in front of you at the security line. But, would you still grant permission to a line cutter if you’re also in danger of missing your own flight?

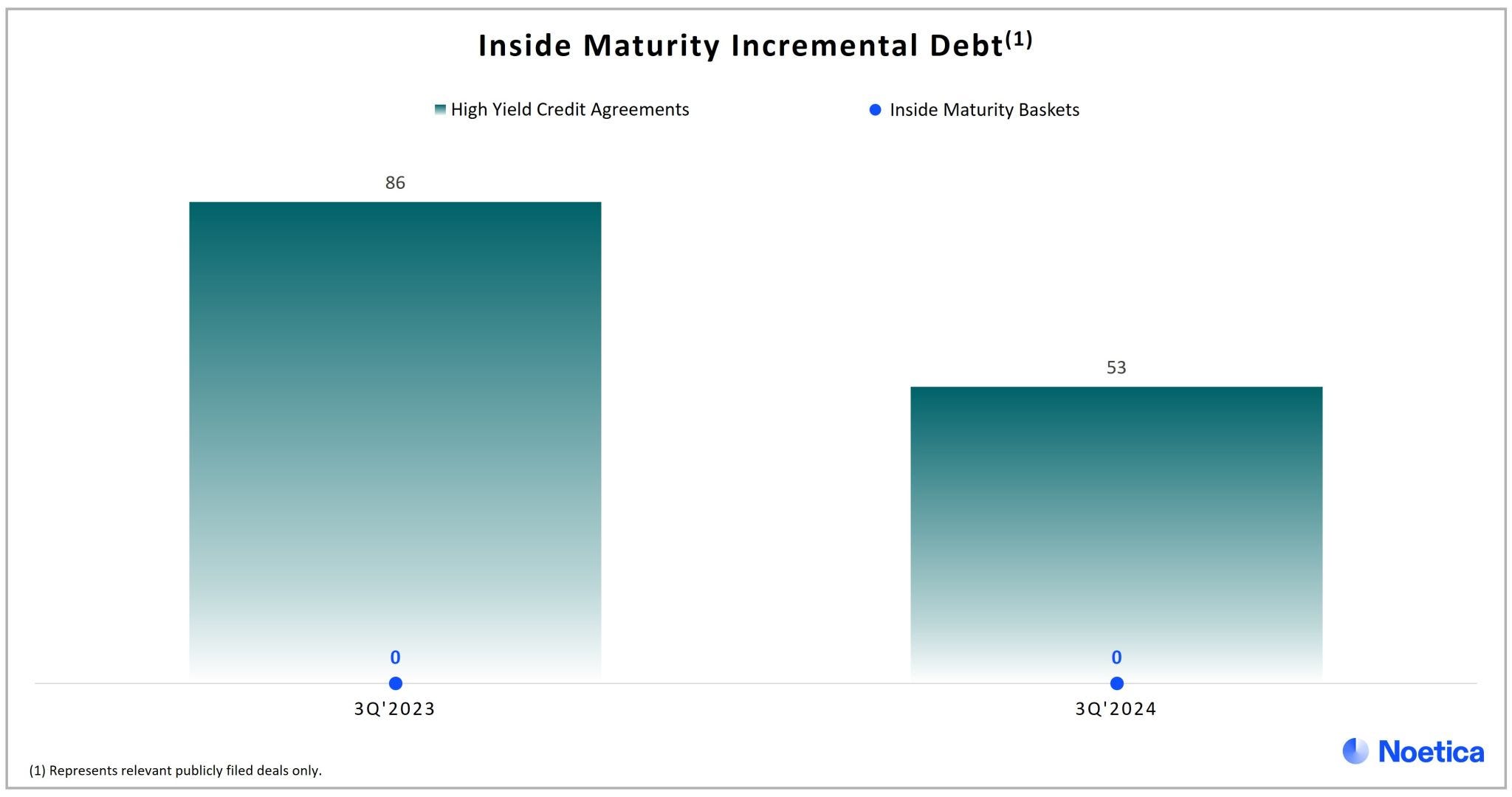

Welcome to the dilemma facing lenders with "𝗜𝗻𝘀𝗶𝗱𝗲 𝗠𝗮𝘁𝘂𝗿𝗶𝘁𝘆 𝗜𝗻𝗰𝗿𝗲𝗺𝗲𝗻𝘁𝗮𝗹 𝗗𝗲𝗯𝘁” in credit deals.

“Incremental debt” terms in new financings permit the incurrence of additional debt while current debt is outstanding. There are many great reasons to permit such activity, including that more capital being available to the borrower typically increases opportunities for growth and decreases the likelihood of a default. However, these terms routinely include a standard requirement: any incremental debt may not have an “earlier maturity date” to the original debt, ensuring that the new debt doesn’t jeopardize the maturity payment for the original lenders.

Importantly, recent deals have introduced an exception to that limitation: an “inside maturity basket” permitting a portion of such incremental debt to mature prior to the original debt in the deal. In other words, if the borrower is in trouble, the “inside maturity” debt will be paid back first, leaving original lenders chasing after an airborne plane.

Every night, Noetica's technology analyzes deal data and adds relevant data points into our knowledge graph of 100+ million deal terms, staying on top of a rapidly changing market—so far, this term change has primarily been confined to private markets: in both Q3 ‘23 and Q3 ‘24, no publicly-filed high yield credit agreements permitted this type of earlier maturing debt.

Message me if you’d like access to the excel with deal data on inside maturity incremental debt.

.avif)