Trend Alert: First Tariff-based Event of Default Pops Up in a Deal—Is This the New Normal?

Trend Alert: First Tariff-based Event of Default Pops Up in a Deal—Is This the New Normal?

Noetica’s AI models unearthed a first-of-its-kind tariff-based event of default term in Superior Industries’ latest credit deal. Is this term an ad-hoc inclusion, or the first of many to come in this new macro-environment?

Background

Superior Industries was a leading manufacturer of aluminum wheels for the automotive industry. Founded in 1957, the company had grown to become one of the world's largest suppliers of these wheels. They design, engineer, and manufacture a wide variety of wheels for both original equipment manufacturers (OEMs) and the automotive aftermarket.

One wrinkle about Superior’s business is that it primarily makes wheels in Mexico for U.S. car manufacturers. Since the administration increased tariffs on U.S. goods imported from Mexico, Superior has struggled to maintain viability, running into a liquidity crunch and significant headwinds in early 2025.

What Happened?

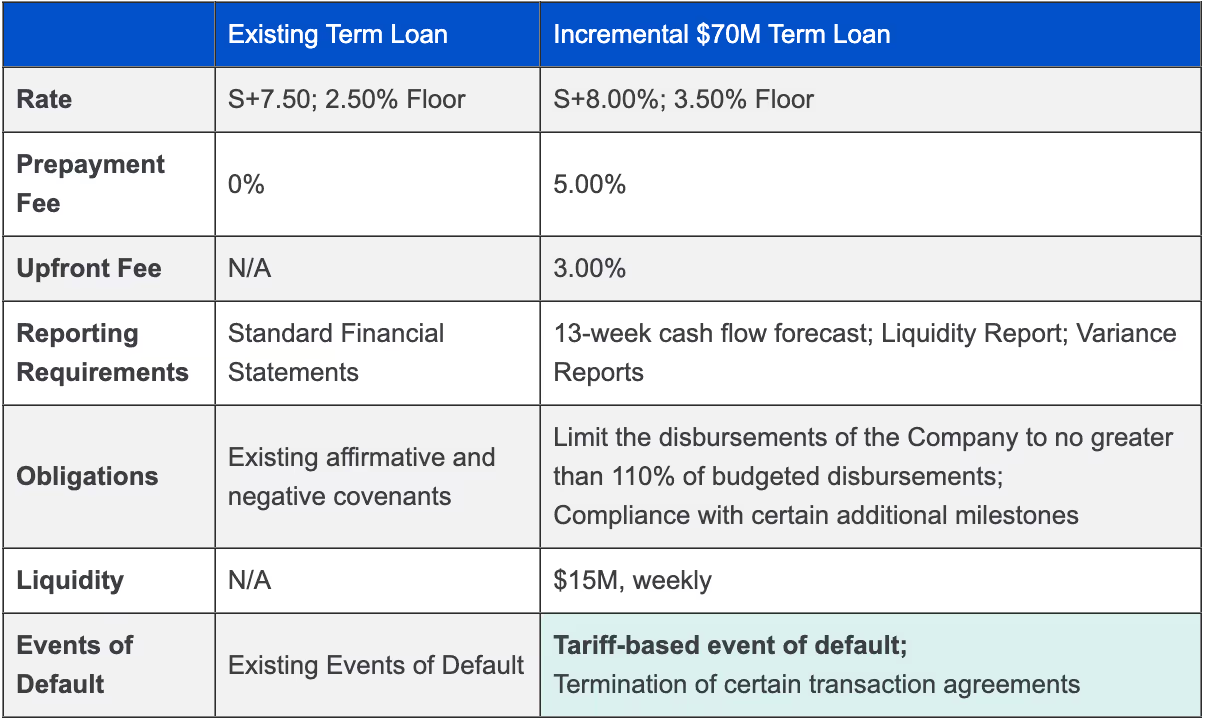

In June 2025, to solve its liquidity crunch caused by new tariff policies, Superior obtained an incremental $70M delayed draw term loan facility through an amendment to its credit facilities, certain key terms of which are highlighted below:

The incremental loan includes the first “tariff-based” event of default in the history of public credit markets (see below). In short, if Superior was subject to tariffs exceeding 20%, and such tariffs could not be passed through to Superior’s customers within 60 days of the levies being imposed, Superior would be in default under their credit facility.

“Tariffs. There occurs any tariffs on any of the shipments of the Borrower or its Subsidiaries into the U.S. exceeding 20.0% of the product value (the “Tariff Threshold”); provided that, if on or prior to the date that is sixty (60) days after the date such tariffs exceed the Tariff Threshold, the Borrower enters into agreements (or otherwise makes arrangements) such that such tariffs are either paid by or otherwise covered by (including as a result of price increases) the customers of the Borrower and its Subsidiaries, then no Event of Default in respect of this section (12) shall be deemed to have occurred;”

Subsequently, on July 8, 2025, Superior announced a significant restructuring and change-of-control transaction, in which Superior would be acquired by a group of its term loan investors, led by Oaktree Capital Management. The restructuring involved a debt-for-equity swap, converting up to approximately $550 million of term loan claims into 96.5% of the new common equity of the indirect parent company. This transaction reduced Superior's funded debt from about $982M to ~$125M, while equity-holders will receive, in aggregate, only $3.1M in cash and 3.5% of the new equity.

Market Implications

Noetica is carefully tracking new tariff-based terms: we’ve now seen both (i) tariff-add-backs in EBITDA definitions, and (ii) tariff-based events of default enter the market. Whether these terms permeate broader quantities of deals remains to be seen, but what is clear is that counterparties are working equally hard to protect themselves from these very real policy threats by building in term mechanics to account for macro changes in such policies.

Noetica’s real-time data and analytics on capital markets terms, is providing instant visibility into how market data is evolving, faster than traditional surveys or anecdotal market intelligence ever could

.avif)